Tilray's Profitability Path Runs Through Canada and Europe, Not the U.S.

Authored by cannabiscanadabuzz.com, 08 Jun 2026

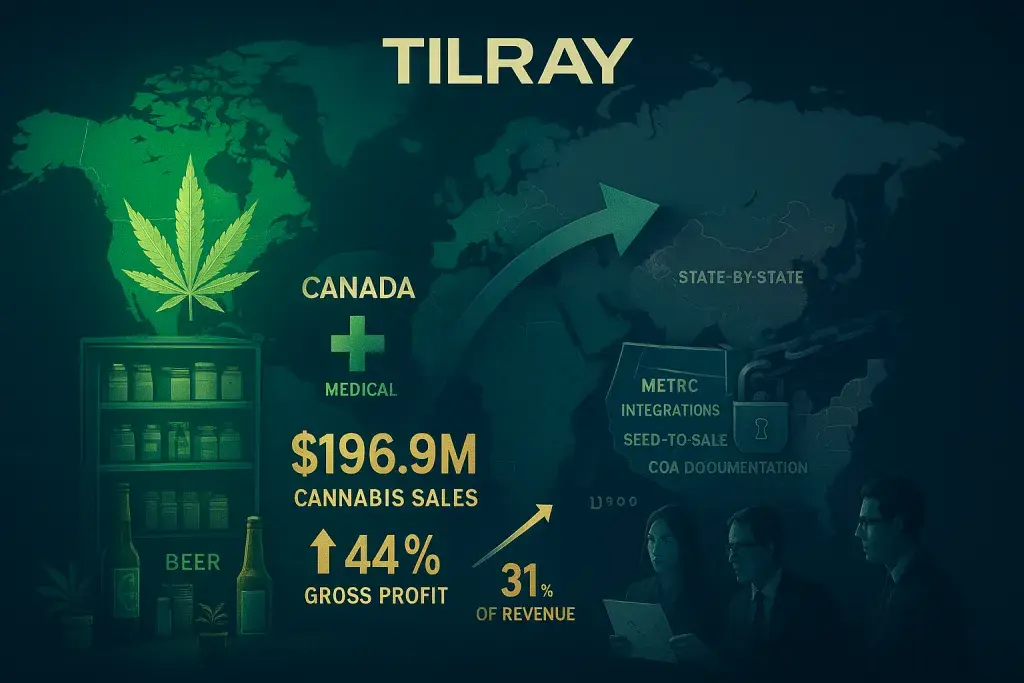

For all the attention Tilray Brands receives as a publicly traded cannabis company, the business case for its stock rests almost entirely on markets outside the United States. Cannabis and hemp-based wellness products together account for 38% of the company's fiscal 2025 revenue - but the cannabis segment alone drives 44% of gross profit on just 31% of total sales. That gap between revenue share and profit contribution tells you something important about where the real margin lives in this business.

The U.S. cannabis market, for all its size and consumer demand, remains structurally inaccessible to Tilray as a revenue driver. Federal prohibition keeps multistate operators and foreign-listed companies in separate lanes. State-by-state licensing, excise tax structures, and compliance regimes - from seed-to-sale tracking requirements to mandatory COA documentation at point of sale - create a fragmented retail environment that adds cost at every layer. Operators using a marijuana pos oregon system, for instance, are working within one of the more mature but still heavily regulated adult-use frameworks in the country, where compliance overhead, Metrc integrations, and inventory reconciliation demands leave little room for error or thin-margin wholesale arrangements. For a company like Tilray, that terrain is largely off-limits at scale.

Canada and the EMEA region - Europe, the Middle East, and Africa - are a different story. Tilray generated $196.9 million in cannabis sales for the first nine months of its current fiscal year from those markets, and those sales carry disproportionate gross profit weight. Canadian adult-use and medical cannabis regulations, while demanding, operate under a single federal framework. European medicinal cannabis markets, particularly in Germany, have been expanding their licensed access programs. Neither environment is simple, but they're coherent in ways U.S. cannabis regulation simply isn't yet.

The Numbers Behind the Non-U.S. Emphasis

Year to date, Tilray's total sales came in at $633.7 million. Nearly three-quarters of that originated outside the United States. What's striking here isn't just the size - it's the direction. Canada and EMEA segments have grown top-line revenue this year. The U.S. and rest-of-world segments have declined. That divergence matters for how investors and industry observers should read the company's strategy.

Tilray reported a GAAP loss of $67.2 million over the period - narrower than the prior year's $913.5 million loss, though that figure was heavily distorted by a $699.2 million impairment charge. Strip that out and the underlying loss compression looks more modest. The company isn't profitable yet, and closing that gap depends on continued growth in its highest-margin segment. That means more Canadian market share, deeper penetration in European medical markets, and disciplined cost management across a business that also sells beer and hemp food products.

What the Beverage and Wellness Mix Actually Means

Tilray's expansion into beverages - beer, specifically - represents a deliberate hedge against cannabis market volatility and regulatory uncertainty. It also introduces a different operational profile: alcohol distribution networks, retail shelf competition, and consumer brand dynamics that have little overlap with licensed cannabis retail. Hemp-based food products carry their own regulatory complexity, particularly around labeling, health claims, and interstate commerce in the U.S. Combined, those two segments generate meaningful revenue but trail the cannabis division on margin.

To put it plainly: the beverages and wellness divisions provide revenue diversification, but they're not what makes the cannabis segment worth watching. That segment's profitability - contributing nearly half of total gross profit - is the core financial argument for Tilray's long-term viability as a public company. Diluting focus away from it carries real risk.

Regulatory Context Shapes Every Strategic Decision

For B2B operators, suppliers, and investors in the cannabis space, Tilray's situation illustrates a structural reality that affects the entire industry: regulatory geography determines financial performance. A company with superior product quality, brand recognition, or distribution infrastructure still can't convert those assets into U.S. cannabis revenue at the federal level. Licensed dispensaries in adult-use states operate under excise tax burdens - including 280E federal tax treatment that disallows standard business deductions - that compress margin at the retail level and reduce wholesale pricing power upstream.

International markets aren't free of regulatory friction, but they offer something U.S. operators often can't: a single compliance framework per jurisdiction. That consistency allows companies like Tilray to scale without rebuilding their compliance infrastructure from scratch in each new market. Until U.S. federal law changes - and the timeline for that remains genuinely uncertain - the profitability calculus for cannabis companies with international exposure will continue to favor those who've built outside American borders first.